Rangeview continued its steady growth trajectory in Q3 2025, reflecting the area’s rising appeal as one of southeast Calgary’s most vibrant and family-friendly communities.

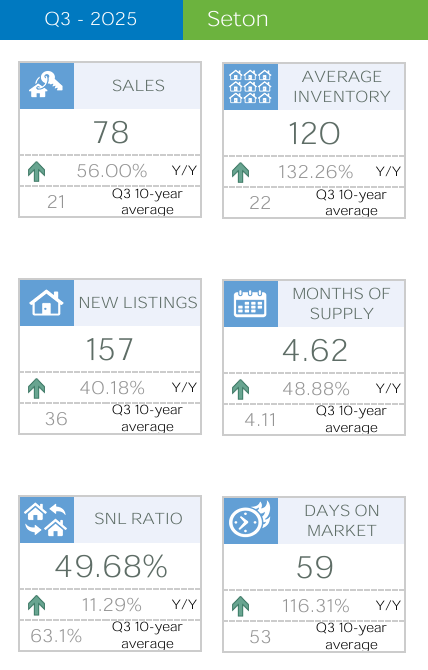

Total Sales: 38, representing a 100% year-over-year increase.

New Listings: 73, up 143% from the same quarter in 2024.

Sales-to-New Listings Ratio: 52.1%, indicating a balanced market.

Average Inventory: 53 units, up 169% year-over-year.

Months of Supply: 4.18, suggesting more selection for buyers compared to earlier quarters.

Average Days on Market: 50 days, slightly longer than last quarter as inventory expanded.

The median residential price settled at $637,950, showing a 1.1% annual decrease, while the average price was $656,954, down 4% year-over-year. Despite minor softening in prices, market activity remained strong across most property types.

Market Trends by Property Type

Detached Homes:

28 sales, up 86.7% year-over-year.

Median price: $661,750, showing a 1.0% annual increase.

Average price: $683,312, down slightly by 3%.

Demand for detached homes remains high, supported by strong new home construction and family migration to Rangeview.

Semi-Detached Homes:

7 sales, a 133% increase compared to last year.

Median price: $630,000, up 5% year-over-year, though the average price dipped slightly to $610,057.

Moderate inventory growth (up over 500%) provided more options, keeping the segment competitive.

Row Homes:

3 sales, up 200% year-over-year.

Median price: $520,000, marking a 4.8% annual decline but still strong relative to other southeast communities.

Average price: $520,373, down 4.7%, consistent with a shift toward more affordable attached housing.

Community Development & Features

Rangeview continues to evolve as a vibrant “agrihood”—a first-of-its-kind community in Calgary designed around urban agriculture, sustainability, and wellness.

Community Gardens & Greenhouses: Residents enjoy access to shared gardens, greenhouse facilities, and seasonal markets, encouraging a strong sense of local connection.

Walkable Design: The community features pedestrian-friendly streets, playgrounds, and future retail zones, designed for family living.

Proximity to Seton Urban District: Just minutes away from Seton Shopping Centre, Cineplex VIP Cinemas, and numerous restaurants, providing all urban conveniences.

Access to South Health Campus: Rangeview is located near the South Health Campus, Calgary’s leading medical facility offering:

24/7 emergency and trauma care

Specialized medical services including cardiac, orthopedic, and oncology care

Wellness, physiotherapy, and outpatient clinics

Research and teaching programs affiliated with the University of Calgary

With expanding housing diversity, rising infrastructure investment, and sustainable community planning, Rangeview is positioned for long-term growth. While price adjustments are moderating short-term gains, buyer demand remains robust, especially among young families and professionals drawn to the area’s modern amenities and proximity to healthcare and retail hubs.

Contact us for a Free Home Evaluation.