In line with seasonal trends, inventory has risen from the start of the year, reaching 6,752 units in May. While these levels are consistent with last May, they remain 11 per cent higher than longer-term trends for the month, thanks to higher supply levels of apartment and row-style homes. Meanwhile, inventory levels for detached homes are down three per cent compared with both last year and long-term trends.

At the same time, sales activity has been slowing. Calgary sales in May were 2,162 units, 16 per cent lower than last year’s levels and similar to sales reported in April. While new listings also slowed by 13 per cent compared with last year, it was not enough to offset the pullback in sales, causing the sales-to-new-listings ratio to ease to 51 per cent. The lower ratio also contributed to some of the inventory build, causing the months of supply to rise. However, conditions do vary across the market, with a range of two-and-a-half months of supply in the detached market to more than five months of supply in the apartment condominium market.

“The shift in supply is being felt in the market. More supply choice in the new and rental markets has created a more competitive environment for potential buyers. At the same time, concerns over rising cost of living and slower migration are also weighing on consumers,” said Ann-Marie Lurie, Chief Economist at the Calgary Real Estate Board (CREB®). “While this has caused the overall resale market to shift to a balanced state, the supply pressure is having a more prevalent impact for apartment-style units, where conditions are favouring the buyer. This is also impacting price movements, with apartment prices continuing to trend down and other property types reporting a seasonal lift over the winter months.”

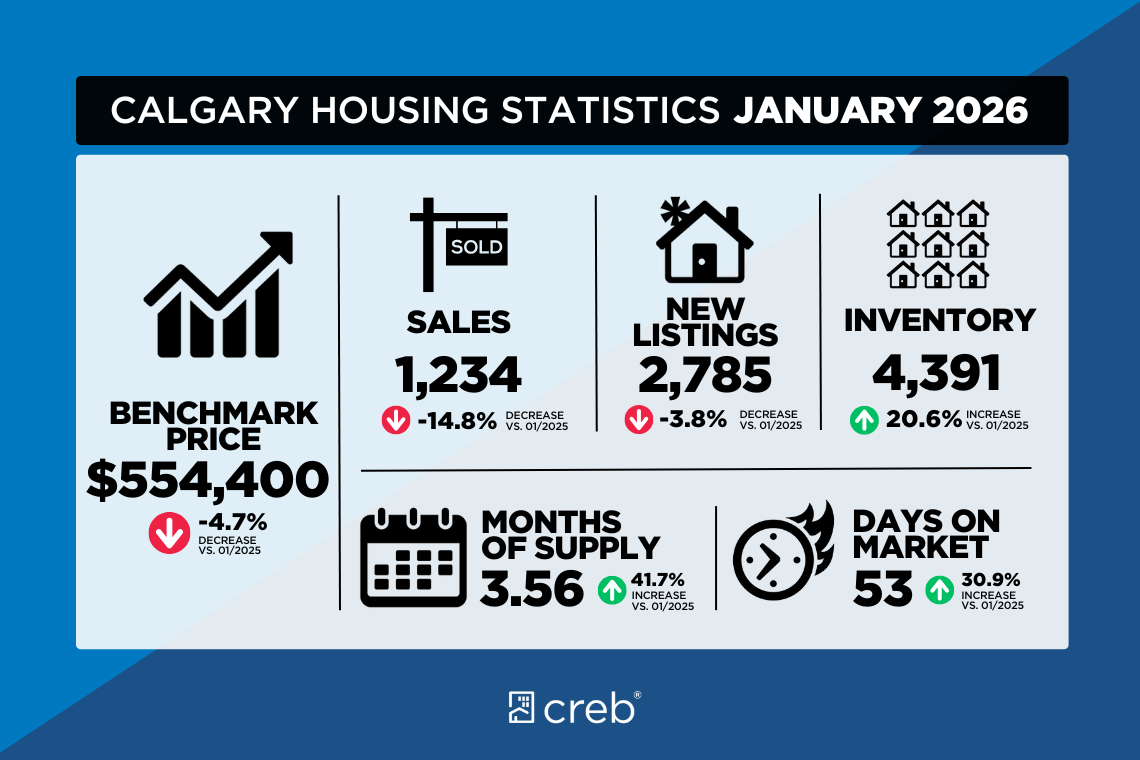

The unadjusted total residential benchmark price in May was $570,500, up over April’s levels and the $554,400 reported in January, but still three per cent lower than last May. Most of the unadjusted monthly gain was driven by detached homes, which rose from $724,000 in January to $747,800 in May. Apartment prices remain lower than January levels and are nine per cent lower than levels reported last May. Overall, when adjusting for seasonality, total residential prices have remained relatively stable, as detached improvements have offset pullbacks for apartment-style homes.

Detached

Detached new listings reached 2,195 units in May compared with 1,192 sales, causing the sales-to-new-listings ratio to ease to 54 per cent compared to the higher levels reported over the past three months. This supported a monthly lift in inventory levels, but supply remained three per cent lower than levels reported last year at this time. With two-and-a-half months of supply, conditions remain relatively balanced and are supporting stability in seasonally adjusted prices. Within the detached market, there is some significant variation. While year-to-date sales have slowed by four per cent, there have been gains for the lowest-priced (under $600,000) and highest-priced ($1.5 million and up) homes. Within each district, conditions ranged from a seller’s market in the West district to a buyer’s market in the North East district. The variation is also impacting price movements. The North East district is reporting the highest year-over-year decline at seven per cent. Meanwhile, thanks to recent gains, the West district has seen prices remain consistent with levels reported last year.

Semi-Detached

Both sales and new listings in May remained at levels similar to the previous month. With 217 sales and 375 new listings, the sales-to-new-listings ratio was 58 per cent, supporting some modest improvements in inventory levels. Despite inventory improvements, conditions remained relatively balanced, with months of supply sitting at just under three months. Unadjusted benchmark prices continued to rise in May, reaching $691,100. This is an improvement over the $667,000 reported in January, but still one per cent lower than levels reported in May 2025. Like the detached sector, conditions vary significantly across the city. Prices have been trending up across most districts. Meanwhile, year-to-date new record-high prices have been reported in the North West and West districts.

Row

Following April’s gains, May sales slowed, adding to the year-to-date decline of 16 per cent. The 350 sales were met with 695 new listings, causing the sales-to-new-listings ratio to fall to 50 per cent in May. This also resulted in slight gains in inventory levels, pushing the months of supply up above three months. While there is more supply compared to several years ago, prices have still reported some modest gains compared with earlier in the year. The unadjusted benchmark price was $422,300 in May. Prices have improved since the beginning of the year, but remain over six per cent lower than last year’s levels. The largest year-over-year declines occurred in the North East and East districts, where prices fell by more than 10 per cent. The West district reported the smallest decline at nearly four per cent.

Apartment Condominium

Additional supply choice in the rental and new-home markets is heavily weighing on resale condominiums. Sales continued to slow into May, contributing to a year-to-date decline of nearly 28 per cent. At the same time, while new listings are not as high as last year, the 403 sales compared to 961 new listings caused the sales-to-new-listings ratio to fall to 42 per cent, keeping inventories elevated. With supply levels remaining elevated and demand easing, the months of supply has pushed above five months, creating conditions favourable to buyers. The excess supply is also weighing on prices, as the unadjusted benchmark price continues to decline. In May, the unadjusted benchmark price was $300,400, lower than January levels and nine per cent below last year’s price. Prices have eased across each district, with double-digit declines occurring in the North East, North, and East districts. The lowest price decline occurred in the North West district at six per cent.