|

|

独立屋市场亮点分析

独立屋市场亮点分析 趋势判断

趋势判断

|

|

|

|

|

|

|

|

|

|

|

Sales: 48 (-14% vs. Q1’s 56). New listings: 76. S-to-N ratio: 63.16% — still a clear sellers’ market.

Average inventory: 20 homes. Months of supply: 1.27 (tight). Median DOM: 18 days.

Benchmark price (all residential): $722,100 (+0.18% QoQ, +0.38% YoY).

Sales mix: Detached = 89.4% of sales; Row/Townhomes ≈ 10%; Apartments = 0% (virtually no condo stock in the quarter).

Prevalence: Nearly 9 in 10 sales were detached, underscoring the lake-community’s single-family identity.

Pricing:

Two-storey benchmark: $764,267

Bungalow/one-storey benchmark: $718,200

Tempo: At 1.27 MOS and 18 DOM, well-priced homes faced multiple-showing weekends and quick offers.

Buyer profile: Move-up families targeting bedroom count, finished basements, and proximity to Mountain Park School and the Beach Club.

Share of sales: ~10% with row benchmark at $425,833; thin inventory means price discovery can be jumpy from one sale to the next.

Buyer profile: Downsizers and first-timers seeking lake-community lifestyle at a lower entry price.

Activity: No apartment sales recorded in Q2; condo options remain scarce in McKenzie Lake proper.

Buyer redirect: Condo shoppers often look to nearby lake-adjacent SE communities when they need this format.

Sellers’ market holds: A 63% sales-to-new-listings ratio with ~1.3 months of supply kept leverage with sellers; small QoQ price gains and sub-3-week median DOM confirm demand resilience.

Seasonality vs. selection: Sales dipped from Q1, but new listings (76) gave buyers slightly more selection—important for move-up purchasers targeting two-storeys near schools and the lake amenities.

What could shift Q3: Any late-summer listing wave could ease bidding pressure; otherwise expect continued stability around the $720k–$770k band for typical family homes, with renovated lake-access properties clearing above.

Family two-storey (most common): $764,267 benchmark. Updated kitchens, A/C, and landscaped yards near school walk-zones drew fastest activity.

Bungalow (downsizer favourite): $718,200 benchmark. Single-level living with modernized interiors remained competitive given limited supply.

Row/Townhome: $425,833 benchmark. When a good one lists, expect swift interest from budget-sensitive buyers.

(Benchmarks are reference points; individual homes trade above/below based on renovation level, lake access, lot, and garage size.)

Beach Club & programs: The McKenzie Lake Residents Association (MLRA) continued spring-to-summer operations and programming at 16199 McKenzie Lake Way SE (Beach Club Hall, outdoor amenities, rentals).

Signature Q2 events:

Father’s Day Fishing Derby — June 15, 2025 (family angling & prizes).

Summer Food Truck Nights, Family Fun Day, Movie in the Park, Summer Send-Off (seasonal community gatherings).

Community Association programming: The McKenzie Lake Community Association ran year-round programs (incl. tots drop-in Sep–Jun) and before/after school care for McKenzie Lake School & St. John Henry Newman (K–5).

Newsletter notes: MyCalgary’s community newsletter reiterates MLRA amenities (tennis, basketball, beach volleyball, toboggan hill) and rental availability of the Beach Club facilities.

Public (CBE):

McKenzie Lake School — K–5; ~560 students; traditional calendar.

Mountain Park School — Grades 5–9; 312 Mt. Douglas Close SE; 403-777-6442.

Catholic (CCSD):

St. John Henry Newman School — K–9; 16201 McKenzie Lake Blvd SE.

Transit: Calgary Transit provides school express routes that many students use for daily commutes.

For sellers

Price tightly off the latest comps for your subtype (two-storey vs bungalow) and launch with complete pre-inspection + professional media; with ~18 DOM medians, your first two weekends matter most.

Consider pre-listing touch-ups that resonate locally: A/C installation, deck refresh, and low-maintenance landscaping for summer showings.

For buyers

Get financing finalized and be “offer-ready” for renovated two-storeys; at ~1.3 MOS, desirable listings don’t linger.

If you’re price-anchored under benchmark, watch the row/townhome segment and be prepared to move quickly when one appears.

Inventory drift: Any late-summer listing bump could nudge MOS toward balance; otherwise, expect steady pricing with slight upward bias in turnkey family homes.

Community draw: Ongoing MLRA events and Beach Club seasonality keep foot traffic high—often translating into stronger weekend showing volumes.

(How much is your home worth? Contact us for a Free Home Evaluation.)

Rangeview, Calgary’s first garden-to-table community, continued to show strong growth through the second quarter of 2025. The mix of detached, semi-detached, and row homes is appealing to a wide range of buyers, from young families to move-up purchasers, keeping demand healthy.

Sales Activity: Q2 posted steady transaction volumes as more new listings entered the market compared to Q1, giving buyers modestly more choice.

Pricing Trend: Home values remained resilient, with modest quarterly increases supported by strong demand for detached homes and stable affordability in townhomes.

Market Balance: Months of supply hovered near 2 months, reflecting a slightly constrained but more balanced market compared to early 2025. Average days on market stayed under 40 days, showing continued buyer urgency.

Benchmark Price: Mid-to-high $700,000s.

Market Notes: Remain the most in-demand segment, especially front-garage homes and those backing onto green space. Buyers prioritize space and proximity to garden lots and pathways.

Trend: Low supply continues to drive competition, keeping prices trending upward.

Benchmark Price: Around $580,000–$600,000.

Market Notes: Attract young families entering the market. Stable price growth, with most homes selling close to list price.

Trend: Balanced performance—steady sales volume but slightly longer days on market than detached homes.

Benchmark Price: Approximately $450,000–$480,000.

Market Notes: Affordable entry option for first-time buyers. Strong investor interest due to rental potential and proximity to future commercial areas.

Trend: Longer average days on market (~45–50 days) compared to detached, but pricing remains steady.

Benchmark Price: Low-to-mid $300,000s.

Market Notes: Limited but growing presence in Rangeview as new multi-family projects begin to develop. Ideal for downsizers or young professionals seeking low-maintenance living.

Trend: Small but steadily expanding segment, with demand tied to affordability pressures.

Commercial Growth: Early phases of retail and dining amenities are under development, with residents anticipating a small commercial hub by late 2025.

Designated Schools: Currently served by nearby communities, including Joane Cardinal-Schubert High School (Seton) and Cranston Elementary.

Future Plans: Land is allocated for future school development within Rangeview, anticipated to serve K–9 students as the population grows.

Nearby Options: Families also benefit from Catholic schools in Cranston and Auburn Bay.

Rangeview Garden Workshops: Seasonal events hosted for residents, teaching urban gardening, composting, and cooking with locally grown produce.

Canada Day Activities: Families gathered in the central park area for children’s games and evening celebrations.

Neighbourhood Nights: Weekly summer outdoor movie screenings and potluck dinners strengthened community ties.

Rangeview is establishing itself as one of southeast Calgary’s most unique lifestyle-focused communities. The emphasis on agriculture and sustainability continues to attract buyers seeking more than just a home, but a community experience. Detached homes remain the strongest-performing segment, but townhomes and duplexes provide key entry points for younger families and investors.

Market momentum is expected to stay strong into Q3 2025, with detached prices leading growth and multi-family development slowly expanding options for buyers.

(How much is your home worth? Contact us for a Free Home Evaluation.)

Inventory levels in June continued to rise, both over last month’s and last year’s levels. By the end of the month, inventory reached 6,941 units, returning to levels reported in 2021, or prior to the surge in population growth. While sales have remained consistent with long-term trends despite a decline from recent months, higher levels of new listings compared to sales have contributed to the inventory gain.

All property types have reported gains in inventory, but both row and apartment style homes reported inventory levels over 30 per cent higher than long-term trends, while supply for detached and semi-detached units are only slightly higher than typical levels.

“Supply has improved across rental, resale and new home markets, allowing for more choice for those considering their housing options,” said Ann-Marie Lurie, Chief Economist at CREB®. “The additional choice combined with no further declines in lending rates, persistent uncertainty and concerns of price adjustments is keeping many potential purchasers on the sidelines. This is weighing on home prices, especially for apartment and row style homes.”

The unadjusted benchmark price was $586,200 in June, lower than last month and over three per cent lower than last year. Much of the citywide decline was driven by apartment and row style homes, which are over three per cent lower than last year. Meanwhile, detached prices have remained relatively stable and semi-detached homes are still slightly higher than last year.

The steeper price declines for apartment and row style homes are reflective of those segments shifting toward a market that favours the buyer with nearly four months of supply. Meanwhile conditions are relatively balanced for detached and semi-detached homes. Overall conditions in Calgary have changed, but not enough to erase the significant growth in prices that have occurred over the past four years.

Sales in June were 1,194 units, six per cent lower than both last year and last month's activity. Sales activity did vary depending on location and price range, with declines in resale sales mostly for higher priced homes that likely face more competition from new homes. On a location basis, the steepest declines in sales occurred in the City Centre and the North East at over 20 per cent, while year-over-year gains were reported in the West, and South East districts.

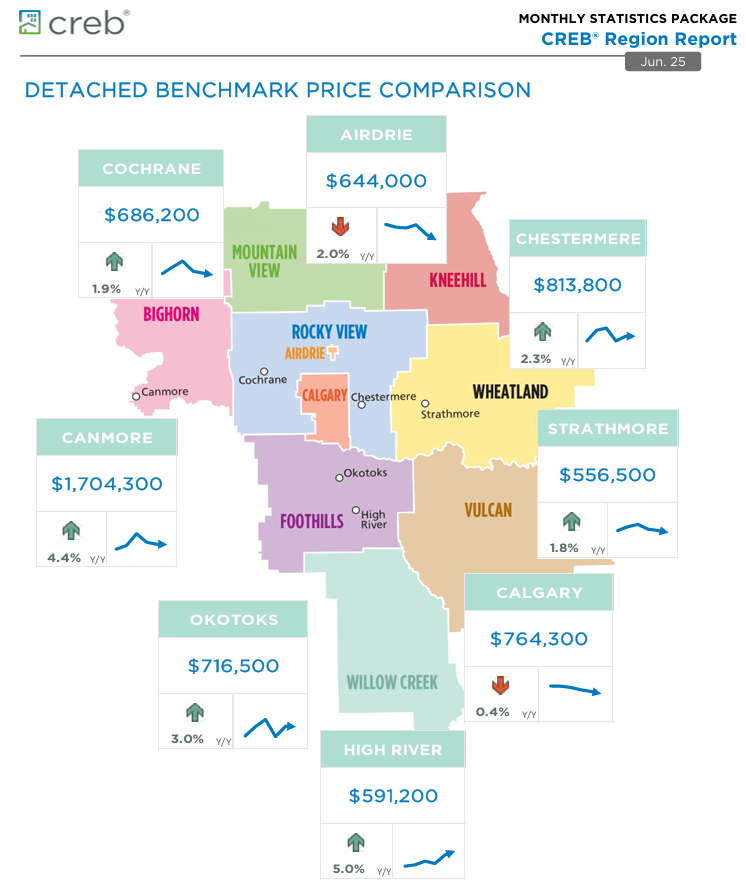

While sales did vary, inventories and new listings improved across most price ranges and districts in the city. However, it is only the North East district that is experiencing conditions that favour the buyer, causing prices to decline by four per cent compared to last June. As of June, the unadjusted benchmark price in Calgary was $764,300, less than one per cent lower than both last month and last year’s price.

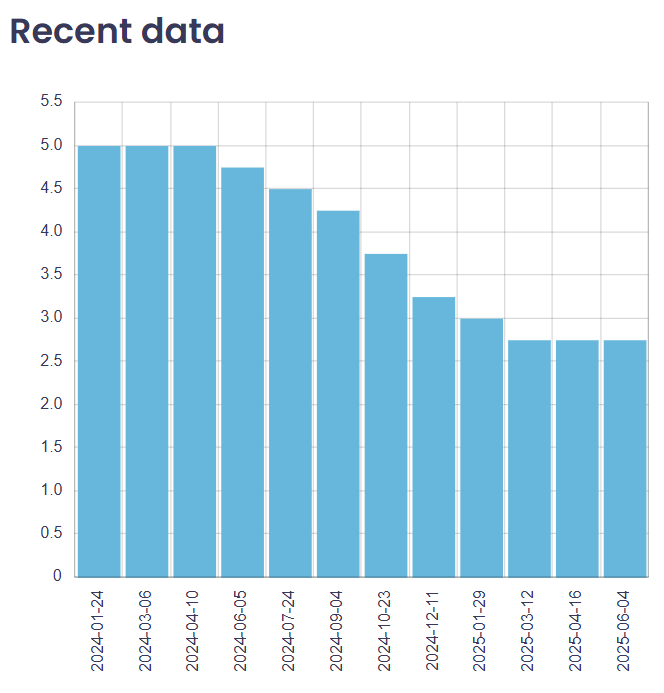

Sales activity continued to slow this month, contributing to the year-to-date decline of nearly 12 per cent. At the same time new listings have generally been rising compared to last year, supporting inventory gains and a shift to balanced conditions. As of June, the months of supply was 2.6 months, a significant improvement over the tight conditions reported last year.

Additional supply choice has slowed the pace of price growth for semi-detached homes. As of June, the benchmark price in the city was $696,400, similar to last month, and over one per cent higher than last June. Price movements did range by district, as homes in the City Centre are over three per cent higher than last year and at record high levels, while prices in the North, North East, and East districts are all over two per cent lower than last year and three per cent lower than last year’s peak price.

New listings continue to rise relative to the number of sales in the market, as the sales-to-new listings ratio in June dropped to 50 percent. This contributed to further inventory gains with 1,167 units available at the end of the month. While sales are still higher than long-term trends, the recent gains in inventory levels have caused the months of supply to push above three months. Within the city, conditions range with nearly six months of supply in the North East and two and a half months of supply in the North West.

Higher supply levels relative to demand are weighing on prices which, at a June benchmark price of $450,300, are down over last month and three per cent lower than last year’s levels. However, as the level of oversupply does range across the districts, so too do the price movements. The City Centre has seen the most stability in prices this month and is only one per cent below last year’s peak. Meanwhile, the North East is reporting year-over-year price declines of nearly six per cent.

June new listings and sales both eased over last month’s and last year’s levels. However, with 1,024 new listings and 532 sales, inventories continued to rise and the months of supply pushed up to nearly four months. Slower international migration numbers are weighing on housing demand just as supply levels are rising, which is having a larger impact on apartment style homes.

The rising supply choice, both in new and resale markets, has caused resale prices to trend down again this month, leaving June’s benchmark price of $333,500 over three per cent lower than last year’s levels. While prices have eased across all districts in the city, the largest year-over-year declines are occurring in the North East, North and South East districts.

Thanks to a sharp decline in detached activity, sales in June fell to 164 units. The pullback in sales was met with 324 new listings, causing the sales-to-new listings ratio to drop to 51 per cent, the lowest ratio reported in June since 2018. The wider spread between sales and new listings drove further inventory gains and for the first time since 2020 the months of supply was above three months. The additional supply choice has weighed on resale prices, which have trended down for the second consecutive month. In June the benchmark price was $538,300, nearly three per cent lower than levels seen last year at this time.

Gains for detached and semi-detached sales were offset by pullbacks for row and apartment units, as June sales remained relatively unchanged over last year. The 101 sales in June were met with 171 new listings and the sales-to-new listings ratio rose to 59 per cent. This slowed the pace of inventory growth, keeping the months of supply just below three months. While conditions are more balanced than they have been, prices in the area continue to rise albeit at a slower pace. As of June, the unadjusted benchmark price was $593,700, nearly one per cent higher than last month and four per cent higher than last June.

While levels are better than last year, both sales and new listings trended down in June, causing the sales-to-new listings ratio to rise to 87 per cent. This prevented any further monthly inventory gains and ensured that the months of supply remained below two months in June. While conditions remain tight in Okotoks, more supply in the broader region has likely prevented stronger price growth in the Town of Okotoks. As of June, the unadjusted benchmark price was $632,800, similar to last month and nearly three per cent higher than last year.

Contact us for a Free Home Evaluation.

Seton remains one of Calgary’s fastest-growing urban districts, offering a vibrant mix of housing, retail, healthcare, and education. In Q2 2025, Seton experienced softening sales and rising inventory — a pattern seen across many SE communities — especially within the apartment market.

Total Sales: 52 units (▼17% YoY)

New Listings: 117 (▼2% YoY)

Total Inventory: 91 units (↑42% YoY)

Benchmark Residential Price (June): $377,467 (▼3.2% YoY)

Months of Supply: 2.63 (↑71% YoY)

Sales: 49 units (↓15%)

New Listings: 111 (↓2%)

Benchmark Price: $377,467 (↓3.2% YoY)

Market Trend: Seton’s apartment-heavy market is cooling. High supply and affordability continue to attract first-time buyers and investors, but price pressures remain downward due to oversupply.

Sales: 3 units (low sample size)

Benchmark Price: Not statistically reliable due to volume

Trend: Limited product available in this category, but ongoing development may expand townhome offerings by 2026.

Not applicable for Q2 2025 – no recorded benchmark or sales activity for these property types in Seton. Most detached homes in the area are still under development or pre-construction.

While specific DOM values are not individually broken out in the dataset, Seton’s months of supply rose 71% to 2.63 months, indicating longer time on market. Buyers have more selection and leverage, particularly in the apartment segment, where competition among sellers is increasing.

Seton is positioned as an education and health hub in Calgary’s southeast. Nearby and serving Seton residents:

Joane Cardinal-Schubert High School (CBE) – Full high school program; modern facility.

All Saints High School (Catholic) – Located nearby in Legacy.

Elementary and middle school students are served by neighboring communities such as Auburn Bay, Mahogany, and Cranston until future Seton schools are completed.

📌 Future School Sites: Designated locations for new K–9 schools have been approved in Seton’s long-term plan to accommodate future growth.

Mixed-use high-density zoning attracts both residential and commercial investment

New apartment and condo developments continue to expand along Seton Blvd and Market Street

Additional park space and pedestrian linkages under development in 2025

South Health Campus Hospital – Full-service medical care and employment anchor

Seton YMCA – Calgary’s largest recreational facility with swimming pools, fitness center, library, and skating rink

Cineplex VIP Theatre, Superstore, Shoppers Drug Mart, banks, clinics, and dining all within walking distance

Apartments remain highly affordable and offer exceptional walkability

Ample inventory and longer DOM provide room to negotiate

Strong rental demand in Seton makes it attractive for investors

Price sensitivity is increasing; units must be competitively priced and marketed

Staging, professional photography, and highlighting Seton’s lifestyle perks are essential to stand out

The oversupply of condos in similar price brackets requires strategic positioning

Q2 2025 marks a cooling phase in Seton’s real estate market, particularly in its apartment sector. While sales declined and inventory grew, Seton continues to hold long-term value due to:

Its position as Calgary’s SE urban center

Access to world-class health, recreation, and retail amenities

Ongoing infrastructure and residential development

Buyers should act carefully but confidently, while sellers will need to align expectations with market realities.

Contact us for a Free Home Evaluation.

Copperfield’s real estate market remained active in Q2 2025, with steady demand across multiple housing types. While sales volumes eased slightly year-over-year, balanced conditions prevailed as new listings rose, giving buyers more selection.

Total Sales: 120 (–9.1% Y/Y)

New Listings: 188 (+11.2% Y/Y)

Sales-to-New Listings (SNL) Ratio: 63.8% (balanced conditions).

Average Inventory: 66 (up 200% Y/Y).

Months of Supply: 1.72 (leaning toward sellers but improving for buyers).

Days on Market: 24 (faster than long-term average).

Overall Benchmark Price: $492,600 (–1.9% Y/Y).

Detached: $624,767 (–0.7% Y/Y).

Semi-Detached: $496,033 (–2.0% Y/Y).

Row/Townhomes: $414,533 (–4.0% Y/Y).

Apartments: $312,467 (–2.7% Y/Y).

Detached homes held values relatively well, while row homes and apartments experienced more pronounced price softening, driven by rising supply.

Detached Homes

Still the most in-demand segment, with 65 sales. Prices held steady, supported by strong family demand and limited long-term supply.

Semi-Detached Homes

Recorded 14 sales. These homes remain a popular mid-tier option, especially for growing families seeking affordability relative to detached houses.

Row/Townhomes

With 30 sales, this segment provides accessible entry points for first-time buyers. Pricing softened, giving buyers more negotiating room.

Apartments

Accounted for 11 sales, reflecting affordability-driven demand. Despite a small dip in pricing, condos remain attractive for investors and younger buyers.

Copperfield is a family-oriented community with convenient access to schools:

Copperfield School (K-5, CBE) located within the community.

St. Isabella School (K-9, Catholic) in nearby communities.

Junior high and high school students are designated to schools in neighbouring New Brighton and Mahogany.

Copperfield is well known for its ponds, pathways, and parks. The community association supports local events and recreation, and the neighbourhood’s access to Deerfoot Trail and Stoney Trail makes commuting convenient. Its balance of affordability and amenities continues to attract families and first-time buyers.

Detached homes expected to remain the strongest segment, supported by family buyers.

Semi-detached and row homes will see steady interest as affordable alternatives.

Apartments may face softer pricing but will continue to appeal to investors and budget-conscious buyers.

Overall, Copperfield should see stable conditions with modest price adjustments as supply levels rise.

Contact us for a Free Home Evaluation.

The New Brighton housing market demonstrated steady buyer activity through Q2 2025, with demand balancing against a healthy increase in new listings.

Sales: 132 transactions (down 13.2% Y/Y).

New Listings: 181 (up 9% Y/Y).

Sales-to-New Listings (SNL) Ratio: 72.9% (favouring sellers slightly).

Inventory: 63 listings on average (up 141% Y/Y).

Months of Supply: 1.43 (indicating a seller-leaning balanced market).

Average Days on Market: 21 (homes selling faster than historical averages).

Overall Benchmark Price: $537,767 (down 1.3% Y/Y).

Detached: $649,967 (–1.2% Y/Y).

Semi-Detached: $547,300 (–2.8% Y/Y).

Row/Townhomes: $420,633 (–0.5% Y/Y).

Apartments: $315,100 (+2.8% Y/Y).

Detached homes dominate the market, while apartments gained traction as affordability pressures grew.

Detached Homes

Represent the majority of sales, with values holding relatively firm. Demand continues from families looking for more space near schools and parks.

Semi-Detached Homes

Pricing softened, reflecting affordability-driven buyer negotiations. Still attractive for families wanting more space than townhomes but at lower costs than detached.

Row/Townhomes

Remained resilient with minimal price decline. With strong absorption, they continue to serve as a popular first-home option.

Apartments

Showed renewed buyer interest, with a 2.8% benchmark increase. Condos are increasingly appealing to first-time buyers and investors seeking entry-level price points.

Families are drawn to New Brighton for its proximity to schools, including:

New Brighton School (K-4, CBE)

St. Marguerite School (K-6, Catholic)

Access to nearby junior high and high schools in Cranston, Auburn Bay, and McKenzie Towne.

South Trail Crossing (130th Avenue SE): Full-service retail corridor with grocery, big-box shopping, dining, and fitness options.

McKenzie Towne High Street: Boutique shops, cafés, and walkable amenities nearby.

New Brighton is a master-planned, family-focused community featuring:

New Brighton Clubhouse: Exclusive resident facility with splash park, skating rink, tennis, and year-round programming.

Pathways & Parks: Ample green spaces, ponds, and playgrounds.

Transit Connectivity: Convenient access to Deerfoot Trail and Stoney Trail for commuting.

Heading into the latter half of 2025, New Brighton is expected to see stable sales and modest price adjustments.

Detached and semi-detached may experience slight downward pressure as supply builds.

Row and apartment segments will likely see continued demand from affordability-driven buyers.

Community amenities, schools, and lifestyle appeal will keep New Brighton highly attractive to families and first-time buyers alike.

Contact us for a Free Home Evaluation.

Auburn Bay entered a transitional phase in Q2 2025, with growing inventory, softer sales volume, and price adjustments across most property types. Although the community remains popular for families, the shift toward a balanced-to-buyer's market created new dynamics for sellers and buyers alike.

Total Sales (Q2): 127 units (↓28% YoY)

New Listings: 238 (↑22% YoY)

Inventory Level (End of Q2): 113 units (↑95% YoY)

Quarterly Benchmark Price (June): $621,467 (↓4.2% YoY)

Quarterly Average Days on Market (DOM): ~25–34 days (↑8–12 days YoY)

Months of Supply: 2.67 months (↑168% YoY)

Total Sales: 54 homes (↓33%)

New Listings: 117 (↑15%)

Benchmark Price (June): $801,633 (↓2.2% YoY)

Average DOM: 32 days

Trend: While detached homes remain desirable, the inventory surge softened prices. Sellers face longer selling timelines unless priced competitively.

Total Sales: 13 homes (↓24%)

Benchmark Price: $524,433 (↓1.1%)

Average DOM: 28 days

Trend: This segment shows moderate stability but slower absorption rates as buyer caution increases.

Total Sales: 33 homes (↑10%)

Benchmark Price: $470,133 (↔ YoY)

Average DOM: 24 days

Trend: A bright spot in the market — row homes are seeing solid buyer activity due to affordability and modern layouts.

Total Sales: 27 homes (↓41%)

Benchmark Price: $359,400 (↓6.3%)

New Listings: 61 (↑72%)

Average DOM: 34 days

Trend: High inventory and weak sales volume place downward pressure on prices. Great value for investors or first-time buyers.

Across Q2 2025, DOM rose across all property types:

Detached homes: From 24 to 32 days

Apartments: From 26 to 34 days

Row homes: Averaging 24 days but beginning to lengthen

This aligns with increased months of supply and softening sales-to-listing ratios — reflecting a more cautious buyer pool.

Auburn Bay continues to be a highly desirable location for families due to its proximity to schools:

Auburn Bay School (K–4, CBE)

Lakeshore School (Grades 5–9, CBE) – Serves growing middle school population

Prince of Peace School (K–9, Catholic) – Popular for Catholic families

Joane Cardinal-Schubert High School – Located in adjacent Seton

Most schools remain well-ranked and accessible via walking or short drive, supporting Auburn Bay’s family-first reputation.

43-acre private lake with beaches, swimming, skating, and boating

Auburn House: Community center, gym, event rental space

Off-leash dog park, tennis courts, and recreational fields

Extensive bike paths and parks throughout the neighborhood

Seton Urban District with:

South Health Campus hospital

Calgary’s largest YMCA

Cineplex, Superstore, and dining options

More selection and leverage, particularly in apartments and detached segments

Opportunities to negotiate price or add conditions

Townhomes remain competitive — act quickly if priced fairly

Prepare for longer DOM and increased competition

Homes in excellent condition, priced to market, are still moving

Professional marketing, staging, and proper pricing are essential in Q3

In Q2 2025, Auburn Bay transitioned toward a more balanced real estate market with:

Declining sales volumes

Elevated inventory

Extended selling timelines

That said, demand for townhomes remains healthy, and the community continues to thrive due to its lake lifestyle, school network, and walkable amenities. Both buyers and sellers must approach Q3 strategically to succeed.

Contact us for a Free Home Evaluation.

Mahogany, Calgary’s award-winning lake community, continues to show steady activity through Q2 2025, with buyer demand remaining strong for both detached and semi-detached homes.

Sales Activity: Mahogany recorded healthy quarterly sales, supported by increased new listings. Inventory improved slightly compared to early 2025, giving buyers more choice, though the market remains tilted toward sellers due to strong demand for family-oriented homes.

Benchmark Prices: Detached homes in Mahogany averaged in the mid-$800,000s, with two-storey properties in particular seeing the highest levels of demand. Semi-detached and row homes remained attractive entry points, with benchmark values in the $550,000–$650,000 range.

Apartments: The apartment sector also posted growth as affordability challenges steered some buyers toward smaller formats. Prices hovered around the low-to-mid $400,000s.

Market Balance: Months of supply remained tight at ~2 months, reflecting the community’s desirability. The average days on market was under 35 days, showing buyers’ willingness to act quickly in this lakeside neighborhood.

Benchmark Price: Approximately $826,800, up around 1.0% year-over-year

April Snapshot: Reflects steady appreciation in this segment

Context: Detached homes remain the flagship offering in Mahogany, especially high-end lakefront and wetland-adjacent homes. They continue to attract families and move-up buyers drawn to spacious layouts and premium finishes

Buyer Insight: Expect consistent demand and resilience in this category, particularly for well-located and well-presented properties.

Benchmark Price: Around $580,500, largely unchanged from Q2 2024

Median Sold Price: $610,000, up 3.4% YoY.

Average Sold Price: $641,373, up from $626,000 the year before

Average Days on Market: 44 days, up from 35 days in Q2 2024.

Sale-to-List Ratio: ~99.3%, slightly lower than 99.7% previously

Buyer Insight: This segment continues to offer strong value — particularly attractive to first-time buyers or those seeking more space than a condo affords. Despite slightly longer days on market, pricing remains stable and competitive.

Benchmark Price: Approx. $498,300, stable year-over-year

Median & Average Sold Price: Both around $349,500, unchanged YoY; slight decrease from $363,000 in 2024

Average Days on Market: 62 days, up from 43 days last year.

Sale-to-List Ratio: ~99.7%, remains steady

Buyer Insight: While sales volumes are low and days on market have increased, townhomes remain an affordable entry point in Mahogany—ideal for first-time buyers or investors. Unit-specific details like exposure and yard access can impact resale and desirability.

Benchmark Price: About $361,900, slightly down (~1.1%) YoY

Buyer Insight: Though pricing has softened a touch, apartments remain a stable, affordable choice—especially appealing to singles, seniors, or those seeking proximity to Seton’s amenities, transit, and health services.

Divine Mercy Catholic Elementary and Mahogany Elementary (CBE) continue to serve young families in the community, both reporting strong enrollment in 2025.

Families also benefit from proximity to Joane Cardinal-Schubert High School in Seton and Centennial High School in nearby Sundance.

A new future middle school site has been earmarked by the Calgary Board of Education, anticipated to relieve demand as Mahogany’s population continues to grow.

With lake access, strong schools, and continued commercial growth, Mahogany remains a premier southeast Calgary destination. Real estate momentum is expected to carry through the remainder of 2025, particularly in the detached and row segments. Apartments will also remain in focus for investors and first-time buyers.

(How much is your home worth? Contact us for a Free Home Evaluation.)

The McKenzie Towne real estate market showed resilience through the second quarter of 2025, balancing demand across a variety of property types. Sales activity remained steady with 132 transactions, a modest 8.3% decline year-over-year, while new listings rose 10.3% to 192, keeping options open for buyers.

Sales-to-New Listings (SNL) Ratio: 68.7% (indicating a balanced market leaning slightly towards sellers).

Average Inventory: 70 listings (up 128% Y/Y, still below the 10-year average).

Months of Supply: 1.59 (suggesting continued demand relative to supply).

Days on Market: 25 (down from 36 historically, showing quicker turnover).

Overall Benchmark Price: $500,633 (down 1.7% Y/Y).

Detached: $652,967 (slight +0.9% Y/Y).

Semi-Detached: $487,933 (–4.1% Y/Y).

Row/Townhomes: $437,600 (–1.9% Y/Y).

Apartments: $332,000 (+2.3% Y/Y).

Detached homes maintained the highest values, while apartments saw price gains, reflecting renewed affordability-driven demand.

Detached Homes

Strongest performer with 65 sales, accounting for nearly half of the market. Benchmark prices held stable, though average sales slipped slightly. Inventory remains tight at under one month of supply for many price points.

Semi-Detached Homes

Softer activity, with pricing down modestly. Semi-detached remain a more affordable entry into McKenzie Towne, appealing to downsizers and young families.

Row/Townhomes

Popular with first-time buyers; stable benchmark pricing despite small Y/Y declines. Good absorption rate kept supply balanced.

Apartments

Increased demand brought sales momentum. Benchmark prices rose 2.3% Y/Y, signaling that buyers are returning to the condo market for affordability.

McKenzie Towne is family-oriented, supported by:

McKenzie Towne School (K-4, CBE)

St. Albert the Great (K-9, Catholic)

Nearby junior highs and high schools in adjacent SE communities.

Proximity to schools continues to fuel demand for detached and semi-detached homes among young families.

High Street in McKenzie Towne: Pedestrian-friendly shopping, dining, cafés, and professional services.

South Trail Crossing (130th Avenue SE): Major retail corridor with grocery stores, big-box shopping, fitness centers, and restaurants.

Seton Urban District (nearby): Expanding entertainment, hospital (South Health Campus), and mixed-use services.

McKenzie Towne remains one of Calgary’s most walkable suburban communities, with village-style planning, ponds, pathways, and community events. These lifestyle features contribute to steady demand across property types.

Looking ahead, moderating price growth is expected as more listings return to the market. Apartments and row houses are likely to see the strongest activity due to affordability pressures, while detached homes remain a long-term draw for families seeking community amenities and schools.

Contact us for a Free Home Evaluation.

While previous generations aspired to enter retirement unburdened by housing debt, a growing share of Canadian retirees are facing a different reality. A new Royal LePage–Leger survey of 1,626 adults, conducted found that 29 per cent—or nearly one in three Canadians planning to retire in the next two years—expect to still be paying a mortgage when they stop working. Mortgage‑free retirement? Not so for 29% of soon‑to‑be retirees (Global News)

Still paying mortgages: 29 percent of near‑retirees (spring 2025) anticipate entering retirement with ongoing mortgage obligations biv.com.

Mortgage‑free cohort: 45 percent have already paid off their mortgage, with another 6 percent confident they’ll clear it before retiring.

Homeownership later in life: Canadians are buying homes later, with amortization schedules (often 30 years) pushing mortgage payoffs well into traditional retirement years globalnews.ca.

Rising mortgage debt among seniors: Canadian seniors with mortgages doubled from 14 percent in 2016 to roughly 28 percent by 2025.

Split on downsizing: Approaching retirees are divided—46 percent plan to downsize within two years of retiring, while 47 percent intend to stay put.

Phil Soper, CEO of Royal LePage, points to housing affordability pressures as a major factor. Escalating home prices, delayed entry into ownership, and financial support extended to adult children have stretched mortgage timelines. While the payoff represents financial liberation and stability, this generation is redefining retirement realities.

Despite the odds, many are finding ways to manage:

Supplemental income sources: Investment earnings, part‑time employment, or support from a working spouse are helping bridge monthly payments .

Financial planning strategies: Advisors suggest delaying Canada Pension Plan withdrawals (until age 70), tapping into investments prudently, or pairing mortgage debt with diversified retirement funding.

The trend reflects broader affordability challenges. The Bank of Canada's housing affordability index reached its worst since 1982, with average homes costing over nine times annual household incomes in 2023. Although interest rates have declined, high prices persist, hampering homeownership .

Plan for mortgage payments into retirement: If you’re close to normal amortization timelines, build mortgage payments into your budget after leaving the workforce.

Delay CPP to maximize income: Eating into your investment portfolio to pay the mortgage may backfire—waiting until age 70 to draw CPP can significantly boost monthly income.

Downsizing: Pros and Cons: Downsizing can reduce expenses and help pay off your mortgage—but only if you weigh factors like moving costs, emotional ties, and future home equity needs.

Consider equity-based solutions: Reverse mortgages (e.g., offered by HomeEquity Bank) allow Canadians 55+ to access home equity without monthly repayments. They can be an option—but total interest may reduce estate value.

What was once a cornerstone milestone—mortgage‑free retirement—has become an increasingly elusive goal. Nearly one-third of near‑retirees now carrying mortgage debt reflects deeper housing affordability issues. But smart financial planning, diversified income strategies, and an openness to options like downsizing or equity loans can help mitigate risks and preserve stability in retirement.

More Real Estate news or market reports, please check here.

Contact us for a Free Home Evaluation.

The Bank of Canada kept its key overnight lending rate at 2.75% again Wednesday.

This marks the second straight hold after the central bank’s rate-cutting streak of seven consecutive reductions ended in April amid the trade war with the U.S. that is wreaking havoc on Canadian monetary policy.

In recent months, the BoC has adopted a strategy that puts more emphasis on assessing short-term impacts, such as economic shocks, economic shocks, rather than usual long-term outlooks when considering whether to hike, hold or cut rates.

The BoC maintained the hold because the bank’s governing council wants to get more information on how U.S. tariffs on Canadian imports could further affect Canada’s economy, BoC Governor Tiff Macklem said during a news conference after Wednesday’s decision.

The hold and Macklem’s comments came on the same day that U.S. President Donald Trump imposed a 50% tariff on steel imports from Canada and a number of other countries, with the exception of the U.K.

“Uncertainty remain high,” Macklem told reporters.

BMO Chief Economist Douglas Porter told The Canadian Press that the uncertainty “really is a doubled-edged sword” for the BoC.

“It doesn’t mean that they should cut more or less,” Porter told CP. “It just makes it more and more uncertain, and they almost have to take it on a meeting-by-meeting basis.”

The hold was widely expected.

First-quarter Canadian economic growth exceeded the bank’s expectation, but compound growth came in as anticipated, Leslie Preston, a TD Bank managing director and senior economist, wrote in a research note provided to Connect. She noted that the economy is softer but not sharply weaker. However, the bank remains concerned about unexpected firm inflation and its preferred measures of inflation have risen.

The BoC also expects the economy to be “considerably weaker” in the second quarter as strong exports and inventories reverse while demand remains “subdued.”

“We expect that barring a trade negotiation miracle with the Trump administration, Canada’s economy is likely to tip into recession this year, and more interest-rate cuts will be required,” wrote Preston.

More Real Estate news or market reports, please check here.

Contact us for a Free Home Evaluation.