By Sammy Hudes, The Canadian Press

As the calendar flipped one year ago, Canadian real estate watchers were optimistic a sluggish 2023 would give way to a rebound, with hopes of renewed demand as soon as the spring.

But the lag in 2024 lasted longer than some expected, with the Bank of Canada waiting until June to deliver the first of the year’s five interest rate cuts. While buyers stormed back to the market this fall, experts noted the first few rate cuts hadn’t been enough to motivate everyone to leave the sidelines quite yet.

Now heading into 2025, economists and real estate agents believe activity is poised to remain strong amid much lower borrowing costs and more favourable rules for buyers, despite an overall challenging affordability picture.

The Canadian Real Estate Association reported earlier this month the number of homes sold in November jumped 26 per cent year-over-year, marking the second straight month of gains at that level. For the first 11 months of the year, cumulative home sales were up 6.9 per cent compared with 2023.

“The big thing is first-time homebuyers are back and are going to continue to get into the market,” said Re/Max Canada president Christopher Alexander in an interview.

“We expect, overall, a much more robust year as far as activity goes and consumer confidence, especially with further anticipated rate decreases.”

The Bank of Canada lowered its policy rate by a half-percentage point earlier this month, bringing it to 3.25 per cent, while signalling a more gradual approach to future cuts in the new year.

Alexander said high interest rates — the central bank’s policy rate stood at five per cent before its cutting cycle — have been a major barrier of entry for would-be buyers.

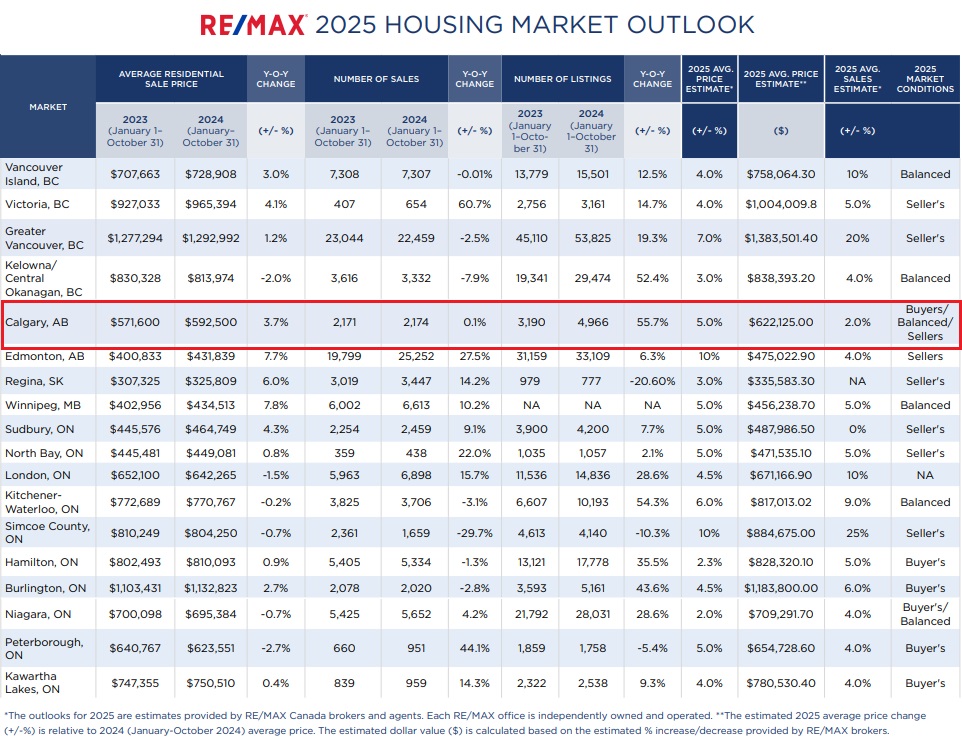

Re/Max’s 2025 housing market outlook report said it is expecting home sales to rise in 33 of 37 Canadian regions, including increases of up to 25 per cent, along with the national average residential price rising by five per cent.

Alexander said the market didn’t really take off after the bank’s first few cuts in part due to messaging that it expected to decrease rates even further as the months rolled along. He said that caused many would-be buyers to hold off “in anticipation of more affordability.”

“But the challenge with that strategy is at a certain point, you hit the point of no return where rates have come down so it’s a little bit less expensive on a monthly basis, but then it becomes more competitive, so prices go up,” he said.

Hamilton, Ont., broker Mike Heddle said for the better part of two years, it’s felt like the “pendulum has swung” from the strong seller’s market of 2021 and 2022.

“There’s just been a real big pause and the masses are just kind of waiting and seeing,” said Heddle of Royal LePage State Realty.

“I’m predicting that we’re going to see a much stronger and resilient 2025 where we’ll probably hover around a balanced-to-a-seller’s market.”

He said buyers’ confidence has been evident in recent weeks, having personally seen an uptick in offers on homes. That could carry over into January after a holiday period that is often fairly quiet.

While pent-up demand should translate to more homes changing hands in the coming months, “it’s not going to be a force forever,” said TD economist Rishi Sondhi. He cautioned that rush will likely be exhausted “relatively soon, probably the first half of next year.”

The national average sale price stood at $694,411 in November, according to CREA.

The initial demand boom should push housing prices higher, though Sondhi noted markets in Canada’s two largest provinces, Ontario and B.C., are still dealing with big supply backlogs that will take time to clear.

Along with falling interest rates, Sondhi said the federal government’s recent mortgage rule changes, which kicked in Dec. 15, should help lift home sales and prices.

Those measures included extending the maximum mortgage amortization period for first-time homebuyers to 30 years from 25, and the cap for which a potential buyer can obtain an insured mortgage being raised from $1 million to $1.5 million.

TD forecasts home sales will rise by 16 per cent across Canada in 2025 on a year-over-year basis, while Canadian average home prices will go up eight per cent.

“You have falling interest rates, you have the likelihood of continued economic growth, and you have these federal measures, all of which should support a good year for housing,” said Sondhi.

Another advantage for buyers is the national banking regulator’s recent move to remove a stress test for uninsured mortgages, said Ratesdotca mortgage and real estate expert Victor Tran.

The Office of the Superintendent of Financial Institutions announced in September it would end the policy for lenders to apply the minimum qualifying rate to straight switches when uninsured mortgages are renewed at a different institution under the borrower’s current amortization schedule and loan amount.

“The spring market will be really hot because of all these recent changes with affordability,” said Tran.

Other factors, such as the labour market and political uncertainty — both domestically and in the U.S. — could play a role in determining the housing picture next year, he said.

But Tran said it’s premature to start comparing the market to 2021 and early 2022 when activity skyrocketed.

“The rates are still not low enough yet compared to what they were before,” said Tran.

“Affordability is improving a little bit, but qualification is still very difficult for a lot of Canadians. So house prices do need to come down a little bit more to really spur a lot more activity.”

For those who find themselves on the verge of entering the market, Alexander said waiting until the perfect time could be a risk in itself.

“You won’t see 2021 activity for a long time. Prices were going up almost by the day,” he recalled.

“I don’t see that happening for a long time, but my advice always is, ‘Buy within your means.’ Timing the market usually ends up in disaster.”

For more Auburn Bay Real Estate market reports, CLICK HERE.