Supply conditions in March varied significantly depending on property type. Inventory levels saw a typical monthly rise, but compared with long-term trends, inventory remained well above the 10-year average for both row and apartment-style units and well below trend for detached homes. This is not a surprise given the pullback in detached housing starts last year despite record-high apartment-style starts.

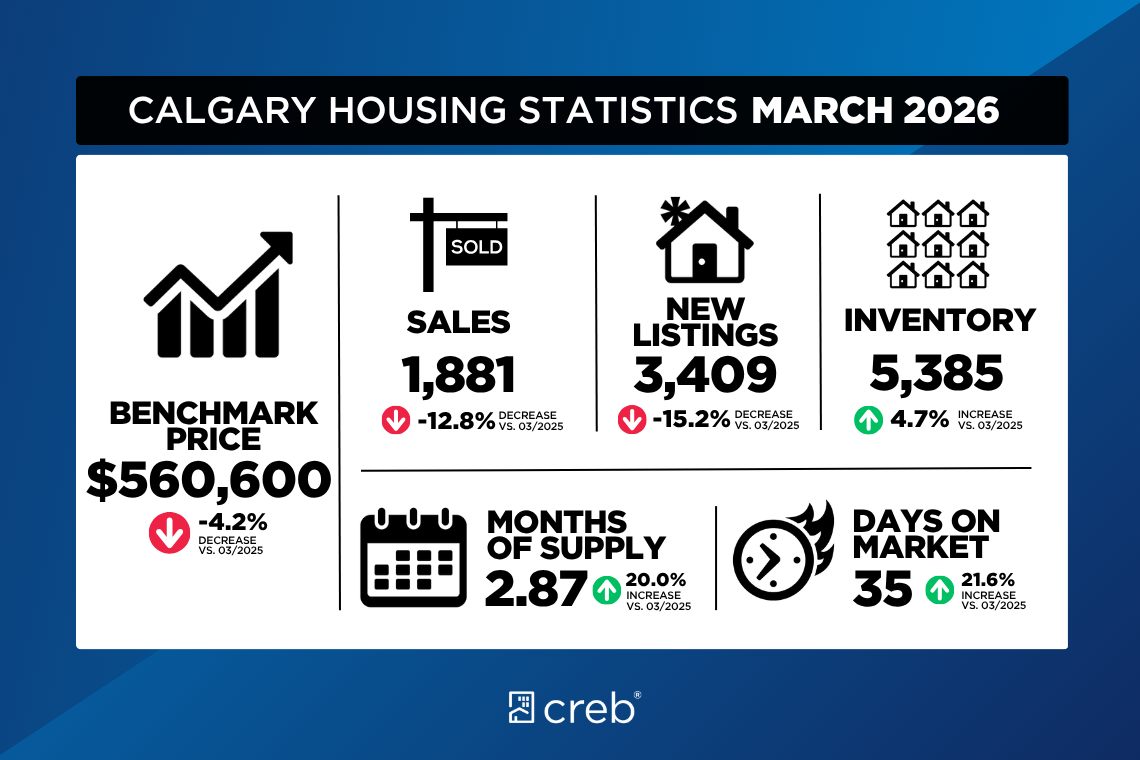

There were 1,881 sales in March, up from the previous month, but still 13 per cent lower than levels reported last year and below long-term trends for March. The decline in sales is mostly due to pullbacks in apartment-style activity, where increased supply choice and slower migration is spreading demand across a wider range of supply. Meanwhile, detached sales have also slowed compared to long-term trends, likely due to limited supply choice in some city districts.

“When considering total residential housing statistics, conditions appear to be relatively balanced as sales, new listings, inventories and prices all trended up over the previous month as we start to move into the spring market,” said Ann-Marie Lurie, CREB®’s Chief Economist. “However, when we look deeper, we are seeing a market that ranges from tighter conditions for detached homes to the apartment sector, where conditions tend to favour the buyer. As expected, this is supporting upward momentum in detached prices and downward pressure in the apartment condominium sector.”

The total unadjusted benchmark price in the city was $565,600, up nearly one per cent compared to February but down by more than four per cent compared to last year. After the first quarter, benchmark prices posted modest to stable conditions for lower density homes. However, apartment condominium prices continued to slide, dropping another three per cent in the first quarter compared to the fourth quarter of last year.

Detached

The detached market is exhibiting the tightest conditions compared to all other property types. With 982 sales and 1,614 new listings in March, the sales-to-new-listings ratio rose to 61 per cent, while inventory levels remained similar to those reported last year. With just over two months of supply, conditions in March closely resembled those seen last year at this time. However, conditions varied across the city, with less than two months of supply reported in the North West, West, South, South East and East districts. Meanwhile, conditions were relatively balanced in both the City Centre and North districts, while the North East district continues to struggle with higher supply relative to demand. The detached benchmark price was $741,300 in March, down by three per cent over last year’s peak price of $766,600. However, tight conditions in most parts of the city are driving some price gains. After the first quarter, the largest quarterly gain was reported in the West district, followed by the City Centre and South districts.

Semi-Detached

Semi-detached sales rose over last year’s levels for the second consecutive month, supported by improvements in new listings and inventory levels. With 480 units in inventory and 193 sales, both levels are comparable to long-term trends and conditions remain relatively balanced. As of March, the unadjusted benchmark price was $686,100—slightly higher than last month and only one per cent lower than last year’s levels. Like other property types, there remains a range in price movements dependent on location. By the end of the first quarter, prices have trended up across most districts, but year-over-year prices remain below last year’s levels in all districts except the City Centre, North West and West districts.

Row

Row home sales continue to slow compared to last year in March, contributing to a first-quarter decline of 19 per cent. The 778 sales in the first quarter were met with 1,581 new listings, keeping the sales-to-new-listings ratio just below 50 per cent and supporting further inventory gains. In March, there were 960 units in inventory — 25 per cent higher than long-term trends — causing the months of supply to rise to nearly three months. While the row market is relatively balanced in most areas of the city, conditions are favouring the buyer in the North East districts. As of March, the unadjusted benchmark price in the city was $423,900, similar to last month and over six per cent lower than levels reported last year. After the first quarter, benchmark prices remain relatively comparable to levels reported in the previous quarter, as quarterly losses in the North East, North, South East and East districts offset the gains reported in the City Centre and West districts.

Apartment Condominium

Supply levels continue to rise for apartment-style units. With 1,774 units in inventory, levels are just shy of the record high for the month reported during the financial crisis in 2008. New supply growth, along with a sharp pullback in sales relative to new listings, has contributed to the rise in resale inventories. With the sales-to-new-listings ratio hovering around 40 per cent and nearly five months of supply, it is not surprising that prices struggle to improve. As of March, the unadjusted benchmark price was $300,300 — slightly higher than last month but over nine per cent lower than last year’s levels. After the first quarter of this year, apartment prices have eased by nearly three per cent compared with the fourth quarter of last year. While prices eased across all districts, the largest declines occurred in the South and North districts, both exceeding four per cent.